For years, a brokerage felt like one product. You opened an account, used the broker's app, held your cash and securities there, placed trades there, received statements there, and thought of the whole thing as a single institution.

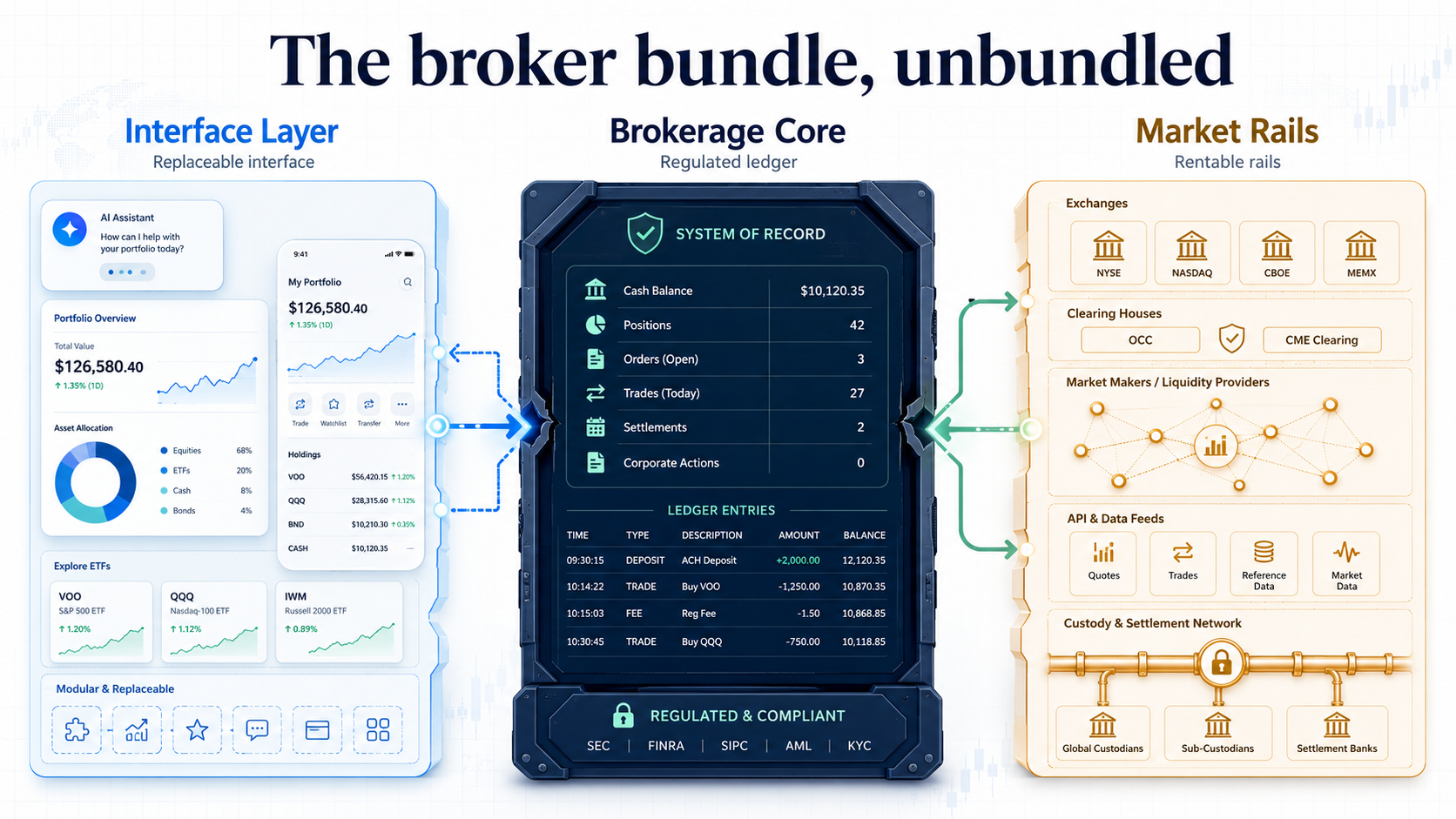

That mental model is breaking. What looked like one product was always a bundle: interface, ledger, execution, custody, compliance, statements, tax records, and market access. The customer only saw the app. Underneath it sat a regulated system of record connecting the user to the market.

That middle layer still matters. In many ways, it is the broker. It records who owns what, where the cash sits, which orders filled, how positions changed, what the customer is allowed to do, and whether the process satisfies regulatory constraints. But the bundle around it is now being pulled apart from both sides.

The right side is becoming API infrastructure

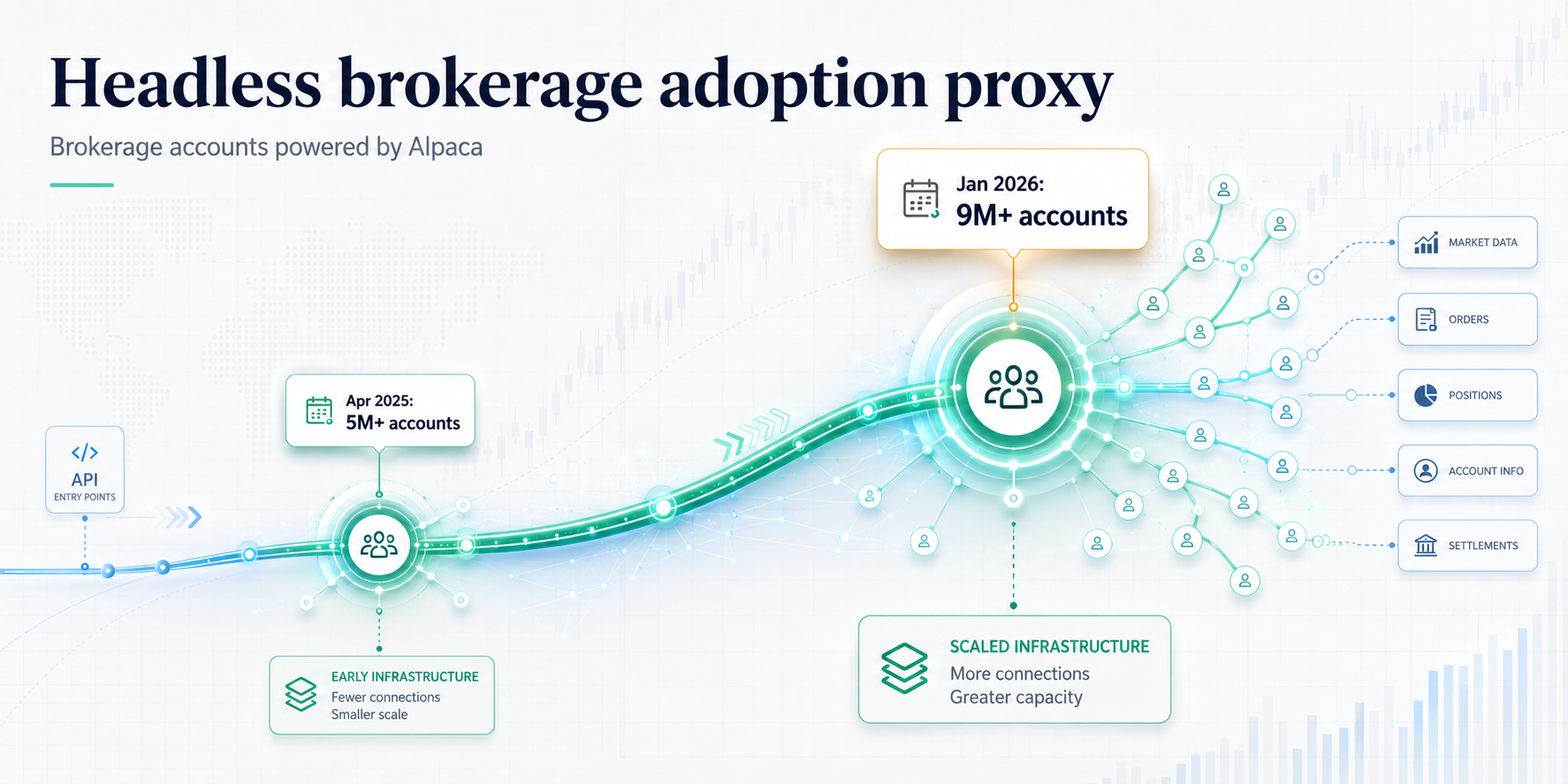

Headless brokerage is no longer an abstract category. In April 2025, Alpaca said it supported more than 200 partners across 40+ countries and powered over 5 million brokerage accounts. By January 2026, it said it powered more than 9 million brokerage accounts across hundreds of fintechs and institutions, while raising $150 million at a $1.15 billion valuation.

The pattern is broader. DriveWealth offers an end-to-end brokerage stack covering onboarding, KYC, custody, execution, tax reporting, books and records, and account types through a single API. Atomic positions itself as infrastructure for fintechs and financial institutions that want to offer brokerage, wealth management, cash management, and custody-backed investing experiences. Interactive Brokers has exposed serious trading APIs for years, but the newer wave is different.

This is not simply "let sophisticated traders connect software to a broker." It is: let another company own the customer relationship, while the regulated brokerage machinery runs underneath.

That distinction matters. Once brokerage operations can be bought as infrastructure, the visible investor relationship becomes contestable. The broker still does the regulated work, but the customer may no longer think of it as the main product.

The left side is being attacked by sharper interfaces

Customers do not wake up wanting "a broker." They want to buy an ETF. Automate an ISA contribution. Understand why a position moved. Avoid sitting on idle cash. Express an investment thesis. Build a portfolio around a goal. Know when something important has changed.

That is why the interface layer keeps splintering into more focused products. InvestEngine has built around low-cost ETF portfolios, managed portfolios, automation, portfolio look-through, and fee-free DIY investing. Trading 212 markets commission-free investing, fractional shares, and automated portfolio "Pies" across millions of funded accounts. Lightyear AI pushes market-move explanations and portfolio-screen intelligence into the workflow. Public now talks about "Agentic Brokerage" for self-directed recurring transactions, alongside AI tools for screening securities with natural language.

J.D. Power's 2025 Wealth Management Digital Experience Study points in the same direction: wealth management apps and websites are doubling down on sleeker interfaces, portfolio analytics, and AI-powered assistants.

None of these products replaces the broker entirely. That is not the point. They compete for the moment that matters most: when the customer decides what to do.

The old broker app was a place to hold assets and press buy or sell. The new interface is trying to become the place where the investor forms intent, understands risk, makes decisions, and automates behaviour. That is a much more valuable position.

The broker bundle is no longer one defensible block

The strategic mistake is to think this is just a UX problem.

That was the 2020 answer: make the app cleaner, reduce friction, add fractional shares, improve onboarding, polish the watchlist. It is not enough anymore.

A good brokerage interface in 2026 has to answer harder questions. What is the user actually trying to achieve? Is the portfolio drifting away from that goal? Is new cash sitting idle? Has the original thesis changed? Which positions are driving risk? What should be monitored next? What can be automated safely? Where does the system need user approval?

Where SIQ fits

SIQ is not trying to be another brokerage skin.

The point is not to make a prettier trade screen. The point is to build the intelligent investment layer above the brokerage account.

That layer should understand intent, turn it into research, translate it into constraints, construct portfolios, monitor what changes, and take action within user-approved boundaries.

The brokerage still matters. It remains the execution, custody, ledger, and compliance substrate. But it becomes the rail underneath the decision layer, not necessarily the place where the customer relationship lives.

That is the value migration. Access becomes infrastructure. The interface becomes intelligent. The intelligent interface becomes agentic.

The uncomfortable conclusion for brokers

Most brokerages will not win both sides.

Running the regulated capital layer is operationally demanding. Building an intelligent, agentic interface requires a completely different product and research culture. The firms that survive will have to choose deliberately.

- Some will become infrastructure. Their customers will be fintechs, banks, wallets, wealth apps, and consumer platforms.

- Some will own the interface. They will make the customer relationship smarter, stickier, and more automated.

- Some will partner aggressively. They will accept that the AI interface layer will not be built like a normal brokerage app.

- Some will get compressed. A mediocre broker app sitting on top of undifferentiated infrastructure is the least defensible position.

The broker does not disappear. The broker gets unbundled. The strategic question is simple: does it own the invisible rails, the intelligent interface, or neither?

Sources

- Alpaca Series C announcement, April 2025

- Alpaca Series D announcement, January 2026

- Alpaca Broker API product page

- DriveWealth full-service brokerage page

- Atomic platform page

- InvestEngine ETF investing platform

- Trading 212 investing platform

- Lightyear AI product page

- Public investing platform and Agentic Brokerage disclosures

- J.D. Power 2025 Wealth Management Digital Experience Study release